Insights On Today’s

Challenges to Homeownership

Challenges to Homeownership

In the current market with today’s state of inflation rising interest rates, slowing sales and higher costs of construction are shouted from the rooftops. Yet it’s important to note that these events are still offset by the outsized demand of a growing millennial age cohort with a need for housing and a slowdown in housing starts that continues to restrict available inventory. Let’s take a look at the data and other counterweights present in the market.

In the Fed playbook the first step to curb inflation such as we have today, involves applying upward pressure on mortgage rates which causes home sales to slow and existing home inventory to rise1a. Yet even with the housing market slowing single-family home inventory has risen only modestly. In July of 2016 listings were noted at 1,468,000 and in October of 2022 they were reported at 753,845, nearly half the level six years ago, and at roughly the same level reported in October of 2020 (733,244).1 In 2021 interest rates were at some of their historic lows and homeowners took advantage to participate in a refinance boom that resulted in over 85% of current mortgage holders with a rate below 5% (Redfin)2. We believe these owners are less inclined to sell their home today and trade for a higher interest rate, which further restrains the rate of rising existing home inventory.

New homebuilders are contributing to this inventory crunch as anticipated, responding to slower sales absorption by reducing starts. According to members of the National Association of Homebuilders (NAHB), in a monthly survey designed to take the pulse of the single-family housing market, the NAHB/Wells Fargo Housing Market Index sits at 38 as of October3(table 1). Anything above 50 is considered positive. Robert Dietz, the NAHB’s chief economist, states: “…given expectations for ongoing elevated interest rates due to actions by the Federal Reserve, 2023 is forecasted to see additional single-family building declines as the housing contraction continues.” 4.

With the 30-year fixed mortgage rates on the rise throughout 2022 and hitting 7% as of late October (since falling back to 6.91% in early November5 and just above the 15 year high of 6.8% in 20066 ) mortgage companies and banks have responded with adjustable rate mortgages (ARMs). ARMs offer lower rates over an initial period of 5, 7 or 10 years7 allowing the homebuyer the ability to purchase today at a lower rate with the option to refinance in the coming years. The annual average rate of an ARM to date in 2022 is reported at 3.99%, although recent rates have trended higher following the trend of the fixed rate mortgage.8 Seeking to maintain options for entry-level buyers, mortgage lenders and banks have implemented or promoted additional steps to improve opportunities for a new home purchase. These include lower down payment loan programs and those that target first-time homebuyers.9

Another factor impacting the housing market has been the high cost of materials and costs of construction resulting from the supply-chain issues instigated in the 2020 pandemic. After months of huge run-ups in basic materials ranging from concrete to lumber, recent reports have indicated some easing on construction costs. As of mid-October prices for building materials have been coming down with lumber down 39.6% since March and steel down 16% over the last four months10. If these essential building materials continue to trend lower, it would ease pressure on builders and buyers alike.

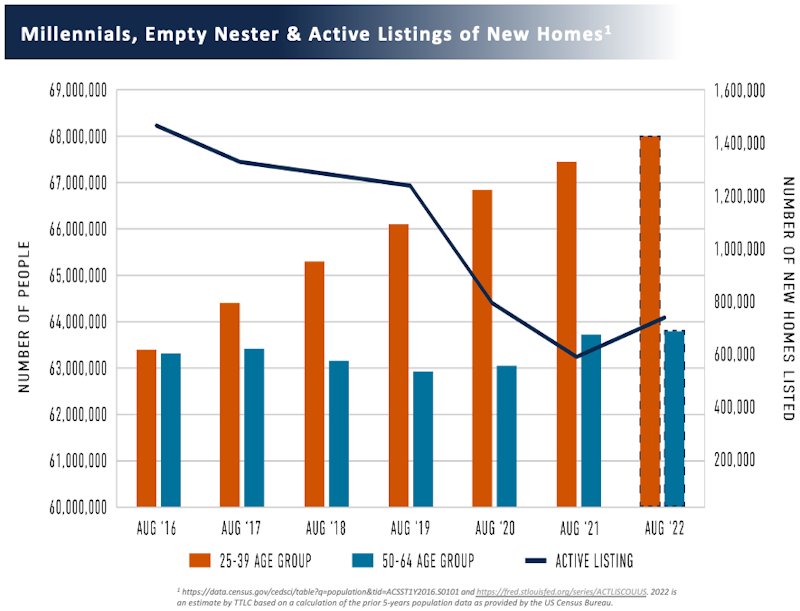

In our analysis, the strongest counter-weight to current housing market conditions is underlying demand. The 26-35 aged cohort of buyers are reaching first-time homebuying age and over the next 10 years, 45 million of the 89 million millennials will reach that age 11 . The millennial cohort, expanded to include 25 to 39-year-olds in the graph at left, is growing year-over-year while the number of active listings has not kept pace. This cohort will continue to be competitive in the new housing market and their desire to own has not subsided.

There is still a need to build new homes for the Millennial and Gen Z cohort that are slowly but surely reaching home buying age. “The share of adults planning a home purchase within a year rose from 13% in the first half of 2022 to 15% in the third quarter.

The marginal increase suggests that the prospect of higher mortgage rates in the near term may be leading a small segment of consumers to consider the purchase of a home sooner rather than later,” writes the NAHB. 12

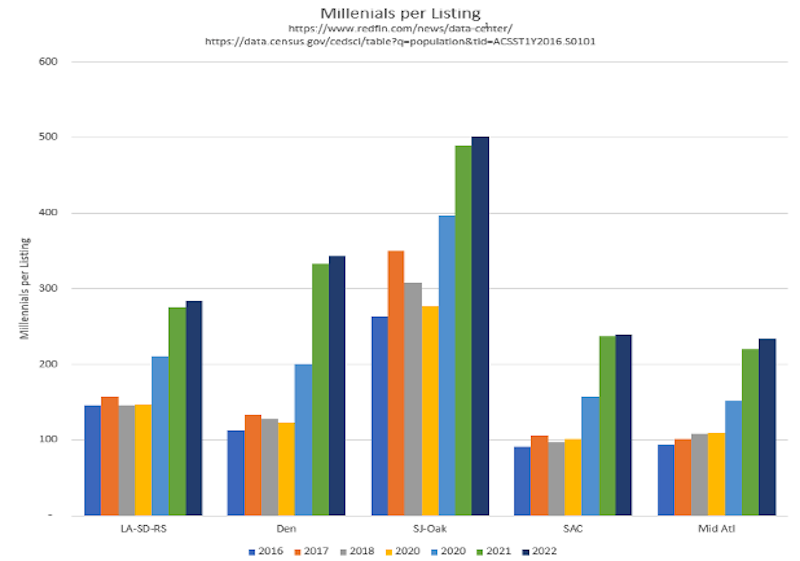

Examining our markets more closely, the evidence of the disparity between the millennial population and the availability of homes for sale illustrates a remarkable divergence. The number of available homes for millennials in TTLC’s markets ranges from just above 225 millennials to 1 home to over 475 millennials to one home, as shown on the table below by region.

“After bottoming out at 19% in the first quarter of 2022, the popularity of new homes continues to rebound, as the share of buyers looking for new construction rose to 21% and 27% in the second and third quarters of the year, respectively,” according to NAHB's Housing Trends Report. This interest is nationwide: The share of prospective buyers looking to purchase a new home rose in all four regions 13.

The United States is drastically undersupplied, short 5.5 million homes according to NAHB, and the more severe underbuilding is happening in the major cities 14. There is demand for new housing in the areas where people want to live: close to work, entertainment, schools, and parks but there is often a lack of available property. In light of current market conditions, property owners recognize they need to adjust their expectations on the price of their property and timing their sale to the market. We are taking advantage of the opportunity presented to our business as a result of these converging factors. As noted by Executive Vice President for The True Life Companies, Scott Menard, “Right now, we are seeing the brilliance of our thesis at work. When others are buying, we are selling. When others are selling, we are buying. Over the past 6 months, we are seeing properties being dropped by other builder/developers, creating opportunities for our company. Properties are coming back to the market with more reasonable price expectations and more favorable terms. We are seeing this across our Regions on deals in Oceanside-CA, Pleasanton-CA, Sacramento-CA, Austin-TX, and Denver-CO right now.”